Operationalising Consumer Duty: why success requires a digital approach to product governance

Day one implementation of Consumer Duty was a monumental and heavily manual task. But ensuring you remain compliant and deliver the right outcomes does not have to be. This first blog in a new three-part series outlines the key criteria for success when operationalising Consumer Duty and explores how firms can make the shift from manual processes to automated systems by making better use of technology.

Customer-centric innovation in financial products has become a prerequisite for growth in recent years. But in today’s tightly controlled environment, where scrutiny is increasing and product regulations are getting stricter, being able to evidence positive customer outcomes is key.In short: innovation in financial services must go hand in hand with effective product governance. Without it, firms can easily end up with unhappy customers, compliance issues, substantial fines, or all three.For firms that are still reliant on heavily manual, outdated processes and systems, this was already a significant – and increasingly expensive – problem. In fact, an independent survey commissioned by Kore last year found more than 40% of senior managers working in financial services experienced product governance challenges when deploying new products or making product changes.Then Consumer Duty made it tougher.

Streamlining Consumer Duty compliance

For many, day one implementation of Consumer Duty was a monumental task. It required a huge programme of highly manual, non-scalable activity, which was time intensive, costly, and nowhere near sustainable.But while there are certainly hurdles to overcome, Consumer Duty also presents an opportunity for the industry.As firms look at operationalising Consumer Duty to ensure they are compliant over the medium-to-long-term it is time to take stock. Now the first step has been taken, there is an opportunity to plan for a future where effective product management and governance is part and parcel of everyday activity and firmly centred around client needs, rather than a periodic upheaval, helping to cement the UK’s leadership role in the global financial services industry.Success will depend on two key factors:

- Modern processes

- The right data strategy

Let’s look at each in turn.

Modern processes: digitising product management

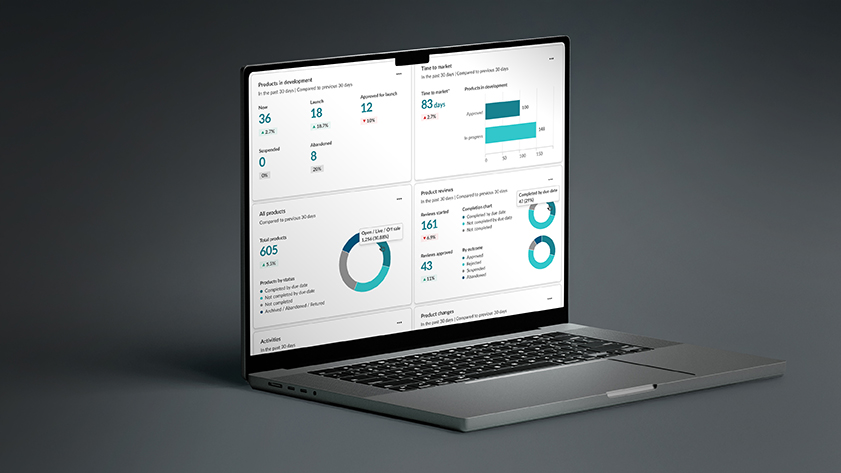

The changes brought about by Consumer Duty require firms to document all stages of the product lifecycle. In other words, a digital audit trail is needed. But doing this with current manual methods is difficult and will likely result in compliance failures.The problem: despite the inherent complexity of modern product governance requirements, many financial firms still build and monitor the corporate history of their products and services across a mix of spreadsheets, emails, and other disparate sources. Data is scattered across the organisation as a result, and all evidencing reviews and approvals must be done manually.

“It is tough to demonstrate compliance in an environment where data is fragmented and there is a heavy reliance on manual processes. The shift we are seeing in product governance today demands a digital layer where all product data can be captured and centralised,” says Josh Blundell, Client Managing Director at Kore.

The solution: a controlled digital environment that acts as the single source of truth, eliminating data silos and creating a smart and efficient way to store and access information on products and services. Not only will this provide regulatory oversight throughout the organisation, but it will act as the foundation for better controls that enable greater visibility and efficiency.

The right data strategy: enabling success with modern processes

While it is virtually impossible to manage all product lifecycle information manually, which is why modern processes are needed, this is only half the battle. To enable organisation-wide success, product information must be considered in the context of a comprehensive data strategy, which means rethinking how data gets collected, stored, and analysed.The problem: data can often be structured differently across each department, or not stored in a consistent way, making it harder for firms to evidence compliance and creating more manual work. Product managers, compliance officers, and their colleagues across the first and second lines of defence cannot exercise their oversight role as a result. They spend too much time gathering data instead of helping the business focus on what matters most.

Modern processes depend on the right data strategy. Only by connecting the two can you truly monitor and drive good customer outcomes. This is where the value of a technology enabled approach, like Kore, comes in. It helps structure data in a consistent, auditable way by giving product a purpose-built home. Firms can then connect the dots to other systems and data sources across the business, bringing the customer and their behaviour into the analysis. This results in dynamic, real-time product management that is truly driven by actionable insight,” says Blundell.

The solution: product data and the events and decisions that relate to them must be connected then organised in a consistent, logical way. This approach helps firms move beyond regulatory checkboxes, creating a streamlined ecosystem where different departments can work together effortlessly.

Technology holds the key

With the FCA estimating that delivering on Consumer Duty could cost the industry £2.4 billion, it is vital that financial organisations meet compliance demands by solving the product management challenges they face. And this depends on making better use of technology.The right technological approach can centralise product design, management, and monitoring so firms can ensure consistency and quality. Front-line staff will gain confidence, too, as they are working with accurate, up-to-date information. At the same time, the optimised resource allocation that results from less manual effort means lower costs and faster time to market. And the better use of real-world data directly connected to product management activity will help deliver good Consumer Duty outcomes. It is a win-win across the board.The question is, what should this look like?Our next blog in this series will look at the options financial firms have available for making this a reality.Have a question in the meantime or want to see how Kore can help you stay up to date with product governance requirements?Get in touch

Thought leadership

The blind spot that could cost you billions: why product intelligence matters

Building trust and a fairer deal for customers: how a digital approach can transform financial services

Operationalising Consumer Duty: how to integrate a product management SaaS solution

Operationalising Consumer Duty: should you buy or build a digital product management platform?

Kore shines a light on financial product governance at EmTech Global